Convergence of “Non-AI” vs. “AI” Investing

Written By Chris Walsh, Partner @7GC

We have discussed, going back to our paper in 2023, how technological revolutions develop from the "big bang" moment through crashes and then, ultimately, the maturity phase.

Since 2022, we have cemented that the Age of AI is here to stay. Across consumers, we continue to see a utilization ramp, with 3.5 billion website visits for ChatGPT in October, representing 101% YoY growth. Across enterprises, there are now 1 Million open-source models, with the top 10 models eclipsing over 1 billion downloads, representing 280% YoY growth. This demand across enterprises and consumers alike has driven cash to continue to flow across the generative AI ecosystem from compute, infrastructure, and application layer solutions. We have highlighted this demand in our piece "AI… and Everything Else":

"As the public markets continue to acclimate to generative AI, private markets continue to show fundraising KPIs that differ dramatically from those of other VC-backed technology cohorts, beginning with total capital deployed. Cumulative funding across private AI companies has continued to be parabolic in the last 12 months, doubling in just 12 months since 2023 and now eclipsing $70 billion."

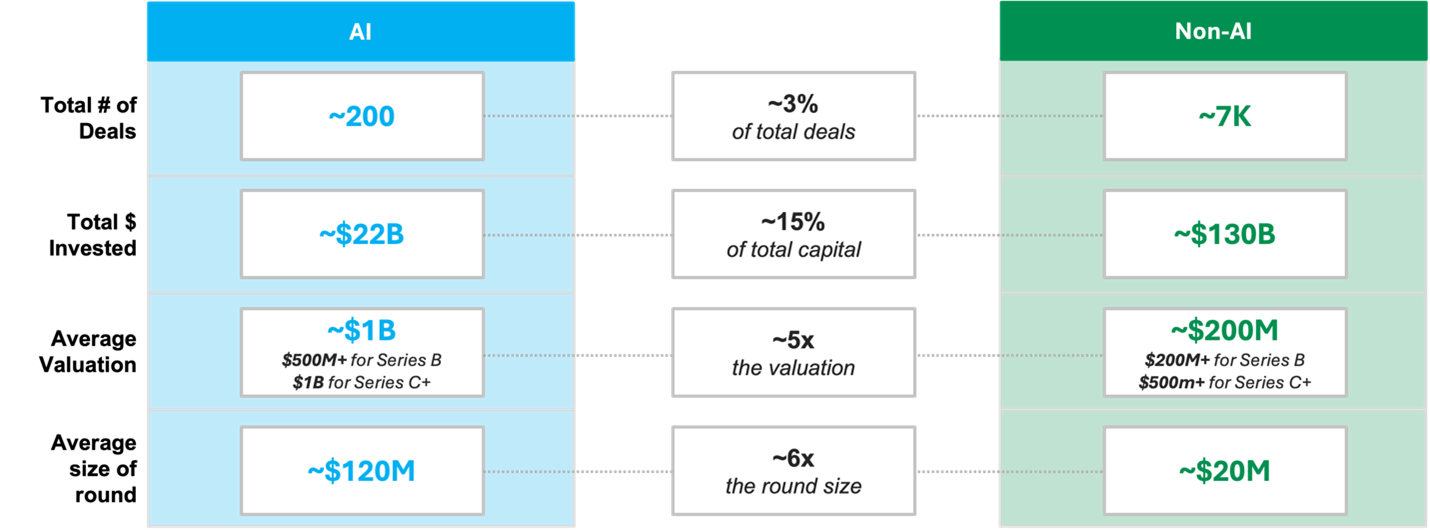

This spending has created a disequilibrium in the venture markets for what today can be coined as "AI" vs. everything else, which we will highlight again to refresh everyone's memory:

Comparison of AI vs. Non-AI Rounds in US YTD

Source: Coatue Management; As of June 2024

The combination of high stakes, consumer exuberance, and broad accessibility of the technology has driven a Goldilocks effect for a new technology era. This concoction has spurred a faster investment deployment period than in previous compute cycles, leading to the average valuation being 5x larger and the round size being 6x larger for generative AI companies than other technology-enabled businesses.

This reality is in line with our general thinking back in 2023 when we stated:

This idea to rapidly race for technological differentiation is best encapsulated by Reid Hoffman with his theory of "Blitzscaling” - “The core idea is to prioritize speed and growth to maintain a market advantage in the modern, tech-driven economy. The commoditization speed for this cycle – based on the broad technological availability of generative AI – challenges this very theory. Incumbents have displayed that they can offer and aggressively market the same AI technology to their existing user base, exhibiting clear-cut challenges to many "AI" startups that have yet to establish a user base or qualified customers. Distribution is costly and takes time, creating - what feels like - daunting business plans for many companies. This was seen in the cloud applications with Slack vs. Microsoft Teams and is materializing already in this cycle with Midjourney vs. Adobe Firefly. Midjourney was launched in July 2022 and Adobe launched an identical product in March 2023."

We have seen this new compute wave blitzscaling at a seismic level led by the magnificent 7 and followed heavily by the venture market. Given the inherent interest of the largest companies with the biggest distribution channels to accept and roll out the technology with incredible speed, we are seeing the technology quickly become "table stakes" across technology teams and even across organizations across all industrial sectors. In previous cycles, when technology became commoditized, it shifted from being a differentiator for new entrants to becoming a necessity for even playing the game.

Today, the companies that are receiving the lion's share of generative AI investments are infrastructure and computing AI apps. As we continue to evolve on the S-curve and adoption continues to move up and to the right, this will transition to the application layer.

Technological S-Curve – Infrastructure to Applications

Source: Coatue, 7GC

The question we continue to receive as investors is how do you split your time between AI vs. non-AI opportunities?

As the infrastructure layer crystallizes and cheapens from chips to the foundation model layer, we continue migrating from implementing/testing products to deployment. This shift from phase 2 to phase 3, will drive a convergence in "non-AI" and "AI" on the application layer. But what does this actually mean?

There has been roughly ~$6B invested in the application layer versus over $45B in the infra layer in generative AI. This gap will narrow and reverse over time, driven by the depreciation of capital intensity and increased company/consumer utilization. This transfer will entirely dilute the bifurcation between "non-AI" and "AI" as in previous compute cycles. In today's world, there is no such thing as a "non-internet," "non-mobile," or "non-cloud" company. To understand when that happened, we first look at the non-AI fundraising trends and then at the convergence cycle in previous compute cycles.

“Non-AI” Fundraising

While this bifurcation of generative AI versus everything else will diminish, the reality is that many core venture verticals continue to show fundraising weakness as tourists fled leaving the specialists ripe to invest in winners unencumbered. While this has been evident across many verticals we track, we aimed to shine a light across the fintech, healthtech, and the e-commerce verticals.

Fintech

Few sub-verticals were aggressively invested in through the ZIRP (zero-interest-rate-policy) era, as was financial technology (fintech). Significant tailwinds existed throughout most of the early 2010s to service customer needs in an increasingly digitalized work, including everyday banking, investment advisory, complex financing, mass wholesale intermediation, and banking as a service (BaaS).

Today, many of these tailwinds have become digested by society, with over 73% of all world interactions with banks now taking place through digital channels. Lending practices also became more broadly accessible across international markets and SMEs in the United States. Low interest rates and unlimited access to venture financing helped drive this rapid adoption. While in hindsight, this seems obvious, there was an obfuscation that current growth trajectories and high-margin businesses in fintech were not subject to macro environment cyclicality, leading valuations to be benchmarked via SaaS comparable multiples. With the rise of interest rates and the ZIRP-era coming to an end, the public markets corrected swiftly.

Fintech Public Market Benchmarks

Source: CapitalIQ, 7GC research; As of 11.14.24

The effects were swift, bringing down growth and corresponding multiple between 70-80% from 2021 averages, with the brunt affecting payments and platforms. This compression has made it virtually impossible for the majority of fintech businesses across Series A-Series D space to raise at a premium valuation. The cause and effect have shown its effect in the private markets within the vertical.

Fintech Private Market Fundraising Trends

Source: Pitchbook, 7GC research; As of 11.14.24

From 2021's peak overall deal flow across the entire venture landscape, deal flow remains on a continued decline across the whole sector, with total deals down 48% from the peak. Later-stage total deal value was hit the hardest– with 2023 and 2024 on track for an 80% decline relative to 2021. The root cause is that many later-stage fintech businesses remain stuck in place with fundraising markets completely inaccessible, given impossibly high watermarks from investors in 2020-2021.

Healthtech

Regulatory capture has impeded healthtech investing historically. The healthcare market is one of the largest addressable markets in the United States, representing over $5 trillion and over 20% of the country's GDP. Despite the scale and many incumbents in the space worth hundreds of billions, there have been limited successful exits across the sector.

During the ZIRP era, many investors seemed to have forgotten or ignored this fact and - coupled with the COVID-19 telehealth boom - helped drive an unsustainable investment bubble across both the public and private markets.

Healthtech Public Market Benchmarks

Source: CapitalIQ, 7GC research; As of 11.14.24

Like fintech, this traversed organically into the private markets with insatiable demand across healthcare services and tangential – and equally regulated – insurance service businesses in the same period.

Healthtech Private Market Fundraising Trends

Source: Pitchbook, 7GC research; As of 11.14.24

Today, deal count continues to fall while total capital remains 60% below 2021 highs illustrating a continued holding pattern and mean reversion to 5-year levels. Given some of the more clear-cut use cases with generative AI and health tech, we are starting to see early signs of troughing in the later-stage cohort within health tech.

While regulatory capture remains intact, the technological shift into AI coincides with younger generations' demographic and cultural shifts. Rex Woodbury framed this phenomenon in his latest post, stating that we are on the precipice of necessary change in the industry.

Wearables and consumables are proliferating across younger generations and legacy B2B relationships are ripe for change driven by telehealth and generative AI solutions. Healthcare runs on medical records, and the LLM / foundational model infrastructure has proven to be best at digesting language at scale, drawing insights faster, and automating actions based on those insights. Unlike nearly all data online, medical records are safeguarded, providing vertically integrated technology companies with a data edge and a pre-existing operating system for health systems. This data MOAT provides a substantial leg up over the new competition - these trends should drive continued demand into leading legacy healthcare startups.

The bonus driver for potential growth is clarity on what a deviated path from the status quo on regulatory capture will be with this new political regime. While it is too early to take a side, we could gain visibility soon on potential winners and losers in both the public and private domains.

E-Commerce

E-commerce has created a fully verticalized ecosystem that continues to increase as we gain better efficiency across the stack, from prepurchase product discovery to post-purchase order fulfillment. While macro drives consumer demand, the continuation of digital gaining market share on brick-and-mortar continues to move up and to the right and remains well below saturated levels that would deter growth.

Within public markets, we saw many high-flying VC startups combust and fail in the public markets following the COVID-19 boom and low-interest rate climate. Many of these businesses were inflating unprofitable growth through unlimited capital and quickly became constrained once the leaky faucet was tightened. Companies like Rent the Runway, Stitch Fix, Casper Sleep, and Blue Apron all struggled, and as cause and effect, you saw massive multiple compression that still exists today.

E-Commerce Public Market Benchmarks

Source: CapitalIQ, 7GC research; As of 11.14.24

You will see that the broader cohort base has shown a strong uplift in the past twelve months, driving multiples in stalking distance of Q4 2021 multiples across our online retail cohort bucket. That figure is deceiving based on the strength of two companies – Carvana (CVNA) and our most significant Fund I investment – hims & hers. If we net both businesses out, the multiple remains compressed ~70% below its 2021 average.

Across privates, various growth vectors like dynamic pricing, targeting, and promotion continue to drive significant data challenges and potential MOATs for businesses. A few themes that have increased and continue to gain momentum that the market has kept an eye on are verticalized platforms, composable commerce, product discovery, and post-purchase transparency products.

E-Commerce Private Market Fundraising Trends

Source: Pitchbook, 7GC research; As of 11.14.24

We still see the deal flow for Series B+ companies down 91% in total deal value, and deals remain on a downward trajectory, down 80% below peaks. Given this data problem, it is unsurprising that e-commerce will be one of the first verticals where AI will enable core efficiencies across the technology stack.

Vertical-Focused Investors Continue to See a Convergence of Non-AI vs. AI Strategies

The data is clear – there remains material weakness for multiples across core verticals, which has trickled down to demand across these private ecosystems, leading to lower deal volume and completed deals despite historic levels of dry powder. In our view, this reality provides a strong opportunity for investors with strong domain knowledge within these verticals offering a rare market timing position to identify clear winners that are best positioned for this AI shift. This convergence will become clearer over the next 4-8 quarters as we continue to shift closer to the application phase of the S-curve, but we continue to be enthused by the strength of early signals.

Generative AI-Associated Deals for Each Vertical Continue to Rise

Source: Pitchbook, 7GC research; As of 11.14.24 Note: Only GenAI deals that were tagged by Pitchbook as generative AI were included

Despite waning or declining trend lines for all three verticals broadly, Gen AI deals continue to move up to the right across all three verticals, with total capital eclipsing over $1B and deal count ramping aggressively in 2023 and 2024 YTD.

To showcase this trend, we looked to evaluate three specialist funds that have a) raised new capital in the past twelve months and b) have a dedicated strategy to a core vertical highlighted below.

Forerunner Capital (vertical focus: consumer / e-commerce):

Focuses on consumer and was founded by Kristen Green in 2010. The firm has backed DTC brands, including Glossier, Away, and Dollar Shave Club. The company announced in 2024 that they have raised $1B for early- and growth-stage investing.

Ribbit Capital (vertical focus: Financial Services):

Focuses on financial businesses and was founded by longtime entrepreneur Meyer "Micky" Malka in 2012. The company has backed credit card startup Brex and the stock trading app Robinhood. The business raised $800M for its tenth fund in 2023.

F-Prime Capital (vertical focus: Healthcare):

Focuses on healthcare services and technology companies and was created as a subsidiary of Fidelity Investments. Their first fund dates back to 2005 and has raised over 16 funds focused on healthcare. The company has backed notable businesses like Ping Identity, Cytek, and Nuance Communications. The firm raised $750M in total to invest across life sciences and healthcare IT and services in 2023.

Tourist Capital Remains Dormant Driving Opportunity

Crossover Investor Investment Levels (2013-2024)

Source: Pitchbook, 7GC research; As of 11.14.24 Note: list of crossover investors represented most active investors that made 20 or more VC investments in period

Tourist capital, or crossover investing, represented over 55% of total deal value across all US VC deal activity in 2021. Given that crossover investing is heavily tilted toward later-stage, those figures are even higher as a % of late-stage investing. As shown above, we have seen a muted return of these investors since 2021, except within generative AI. ~25% of all capital invested by these investors was funneled into generative AI deals, representing over $8.8B in total deal value.

Removing tourist capital, we see two key trends common for vertical specialists across all three highlighted verticals. For one, we are beginning to see a convergence of generative AI use cases merge into vertical-specific solutions, with these investors leading many of these rounds. On a weighted average basis, ~47% of all deals made in 2024 had an associated generative AI theme wrapped around the investment.

Composition of Deals with Generative AI Theme in 2024

Source: Pitchbook, 7GC research; As of 11.14.24 Note: 7GC analyzed and reviewed each investment made by each firm in 2024.

The second, coinciding with point one, is an uplift in the number of investments made by these investors. We continue to see a healthy uptick to a 10-year normalized deal flow level for each of these vertically-focused investors:

Deal Count by Firm (2014-2024 YTD)

Source: Pitchbook, 7GC research; As of 11.14.24

The early signs of vertically-focused investors investing in application-layer businesses within their designated industry show that what started as an infrastructure-focused investment focus for generative AI is organically moving into the application layer, thus promoting fresh deal flow for these investors.